March 8, 2024

Supply & Demand: Aviation Market Analysis

by Konrad Blocher | VP Sustainability & Strategy

After years of insufficient demand caused by the global COVID-19 pandemic, the aviation world is suddenly struggling with a different imbalance – not enough aircraft. This has several consequences across the industry, starting from packed aircraft and routes being cut through high aircraft rentals and market values to manufacturers cashflow disruptions. Understanding the cause of the imbalance is therefore key to trying to explain the next few years.

Obviously, there is a multitude of drivers of the balance of supply and demand in the industry, but we will focus on one specific item here – identified in our previous research as key in driving the market of commercial aviation. This simplified analysis sheds some light on the scale of our current challenge.

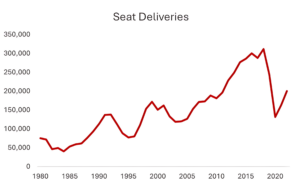

Aircraft get delivered into the stock of commercial aircraft and stay there for a long time (their economic lives being ca. 25 years) and therefore the number of seats delivered into the system has a huge impact on the market. The chart below shows the number of seats delivered into the industry from 1970 until last year.

Source: mba aviation analysis

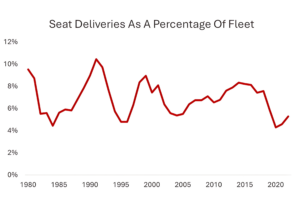

We see both exponential growth and cyclicality as well as the impact of post-COVID production cuts, but to analyse deliveries in a consistent manner, we need to compare them to the world’s embedded fleet.

Source: mba aviation analysis

This comparison enables us to remove the growth element and focus on the element we set out to investigate – cyclicality. We need to account for the long-term average number of deliveries – ca. 6.9%. This figure is representative of the number of aircraft seat deliveries that satisfy both replacement and growth demand and keep aircraft economic life at historical averages.

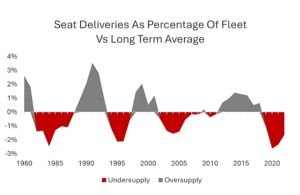

Source: mba aviation analysis

We see periods like the late 1980s, early 2000s and 2010s where manufacturers delivered more than was historically required and periods like early 1980s, late 2000s when production cuts contributed to significant undersupply of new aircraft seats.

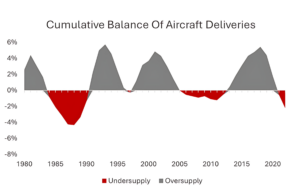

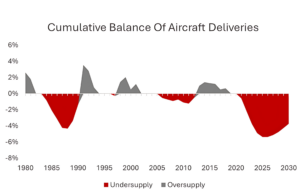

As discussed above, aircraft stay in service for a long period of time, which suggests we should focus on a cumulative number of deliveries rather than point in time measurements. When we translate the chart above into a cumulative sum of deliveries vs trend we get the following relationship.

Source: mba aviation analysis

This chart explains the current state of affairs quite well – we see a shortage of aircraft as demand for air travel is returning towards historical trends. That delivery-driven shortage is exacerbated by other significant disruptions (like the GTF HPT inspections) that are not captured here.

Looking into the future, we can combine manufacturer delivery schedules with an expectations of demand rebounding and achieving levels close to pre-pandemic trends. This allows us to forecast the supply and demand balance conditions over the foreseeable future.

Source: mba aviation analysis

We can see that the general balance will tighten over the next few years. Naturally, changes to forecasts of future demand would impact the situation as will significant movements in manufacturer production rates. However, we do see the general market conditions being quite tight for airlines with upward pressures on values and lease rates.

For questions or comments regarding this insight, reach out to the author, Konrad Blocher, at kblocher@mba.aero to discuss further.