May 28, 2024

Narrowbody Engine Values as a Proportion of Aircraft Values

by Sloane Churchill | Manager of Asset Valuations

An important topic of conversation this year has been engine value as a percentage of total aircraft value for new technology aircraft, with the sharpest focus placed on the A320neo and 737 MAX families. Pricing increases for new technology narrowbody engines, including the PW1100G, LEAP-1A, and LEAP-1B, has been strong over the past two years. These increases are driven by several factors.

Firstly, there has been double-digit escalation in new engine OEM list prices and published maintenance costs, including life limited parts (LLP) and engine performance restoration costs. Secondly, ongoing technical issues have caused increased inspection and maintenance requirements, leading to backlogs at MRO shops, and continued supply chain challenges, driving up spare engine demand. Production delays and durability issues have also severely limited the availability of serviceable spare engines in the market to meet that demand. This is particularly true of the PW1100G engine as a majority of the fleet is going through the inspection and repair cycle for powdered metal production issues, grounding hundreds of aircraft at a time. As a result, not only have Market Values and Lease Rates for the types increased over the last few quarters, but Base Values have been impacted as well. As these engines are early in their life cycles, and list pricing and maintenance costs are increasing at elevated rates, Base Values are appreciating faster than originally forecasted for the types. In 1Q 2024, mba made positive Base Value adjustments to these engine types in order to keep up with pricing escalation.

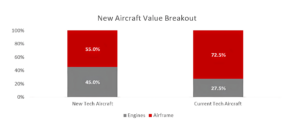

Based on mba’s 1Q 2024 published engine and aircraft values, the Market Value of two new technology engines currently accounts for approximately 45.0% of the value of a new aircraft delivered in January 2024. Looking at a PW1127G-powered A320neo, for example, the engines make up 50.5% of the Market Value of a new aircraft, and two LEAP-1A26 engines make up approximately 42.9% of the Market Value of a new A320neo. The PW1133G makes up 49.2% of the Market Value of a new A321neo, with the LEAP- 1A33 making up approximately 43.8% of the Market Value. On the 737 MAX 8, two LEAP-1B27 engines make up approximately 42.0% of the Market Value of a new aircraft. This generational shift in the makeup of the value of a new aircraft is significant as historically, in the case of the ceo and NG families, engines comprised approximately 25.0-30.0% of the value of a new aircraft.

Source: mba REDBOOK, 1Q 2024

This shift in the makeup of the value of an aircraft has to do primarily with list pricing, maintenance costs, and differences in escalation rates for spare engines versus new aircraft. New technology narrowbody engines are more expensive than their predecessors, with higher list prices and quickly escalating maintenance costs driving value. Additionally, engine OEM escalation is typically higher for spare engines than for full aircraft campaigns.

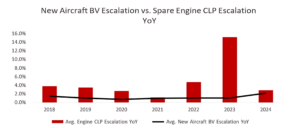

Historically, mba’s new aircraft Base Values for A320neo and 737 MAX family aircraft have escalated on average 1.0% year over year since 2018, though this has increased to upwards of 3.0% in 2024. Meanwhile, OEM published engine list prices for LEAP-1A, LEAP-1B, and PW1100G engines have escalated on average 3.0% – 5.0% year over year since 2018, but saw an average 15.0% uptick in 2023, leading to potentially unsustainable values curves. PW in particular escalated list prices approximately 25.0% in 2023 while the LEAP-1A/1B list prices escalated approximately 8.6%.

Source: mba REDBOOK, 1Q 2024

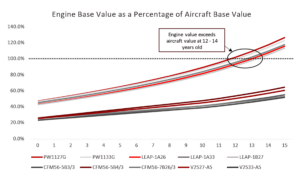

Over the aircraft’s life cycle, engines make up an increasing proportion of the value of the aircraft. As engine Base Values appreciate through the early part of their life cycle and the aircraft value depreciates over the same period, there will be a point where the value of two engines exceeds the value of the whole aircraft. Typically, this happens later in an aircraft’s life cycle when production has ended, and aircraft are beginning to be retired and become part out candidates.

For current generation narrowbody aircraft, engine Half-Time value would be expected to exceed total aircraft Half-Time value when the aircraft is around 20 to 25 years old. However, for a new technology narrowbody aircraft, the value of two Half-Time engines is forecasted to exceed the value of the full aircraft by the time the aircraft is 12 to 14 years old, based on Future Half-Time Base Value curves derived from historical depreciation rates. Using this same methodology, by the time an aircraft is five years old, the Half-Time value of two engines makes up approximately 61.3% of the value of the aircraft, compared to 33.1% of the value of a previous technology aircraft.

Source: mba REDBOOK, 1Q 2024

Market Lease Rates tell a similar story to Market Values. The cost to lease two new technology engines, excluding utilization fees or maintenance reserves, is approximately 91.0% of the cost to lease a new aircraft. In the case of the PW1127G on the A320neo, the cost to lease two engines actually exceeds the cost to lease a new aircraft by approximately 4.0%. Lease Rates for the remaining engine and aircraft combinations generally hover around 80.0% – 90.0% of the Lease Rate for a full aircraft. While Market Lease Rates are currently elevated due to supply and demand imbalances, it is likely they will continue to make up a majority of the Lease Rate for a full aircraft over the near to medium term while the aircraft are still in production.

Source: mba REDBOOK, 1Q 2024

This value trend has potential long-term implications for the future of A320neo and 737 MAX family aircraft. Not considering any airframe value, new aircraft are potentially part-out candidates by the time they finish their first lease, assuming new technology aircraft values follow a similar depreciation curve as their predecessors. While this may appear to be a possible scenario, mba does not expect to see increased rates of retirements and part outs for these aircraft this early in their life cycle. The industry is experiencing a shortage of narrowbody aircraft that is expected to continue into the next decade as OEMs struggle to ramp up new aircraft deliveries and domestic traffic demand growth exceeds 2019 levels. This shortage is keeping previous technology aircraft in service longer than planned, stunting retirement rates, which is likely to continue in the short to medium term. Additionally, due to passenger traffic demand, new technology aircraft are not expected to be parted out en masse at a young age, but rather see strengthened Market Values.

Engine Market Values and Lease Rates are also expected to begin stabilizing as the engines enter technical maturity and more spares enter the market to mitigate the current demand imbalance. Within the next 20 years, engine Base Values will begin to depreciate as the engines enter the mature phase of their life cycles, which may help mitigate this trend in the long term. There could be further long-term implications should a clean sheet narrowbody replacement enter the market, which may accelerate depreciation and shorten the life of the engines and aircraft. There are no clear answers as of yet how new technology aircraft will be affected by the shift in composition of value, but this trend is one mba is keeping a close eye on moving forward.

If you have any questions or would like to discuss any of mba’s commentary above, please contact Sloane Churchill at schurchill@mba.aero and David Archer at darcher@mba.aero. mba’s full appraisal team can also be reached at appraisals@mba.aero.