August 2023

737-800 MARKET PROFILE

Historical Values

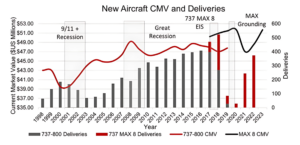

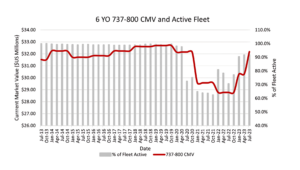

Market Values for the 737-800 show a gradual increase over the first 10 years in service and have been resilient even after declines during events such as 9/11, The Great Recession and the pandemic. The 737-800 CMVs took around 2 years to bottom after each initial event before recovery began, with the exception of 9/11 when values began to recover almost immediately.

Positives

+ The grounding of the MAX 8 briefly boosted values of the 737-800 in 2019, but values declined soon after due to the pandemic. Three years later, values have shown strong signs of recovery, which is slightly longer than previous downturns but faster than other previous gen aircraft post-pandemic.

Neutral

○ Once production levels peaked, values remained flat, yet stable for the remainder of the aircraft’s production run.

Negatives

– 2008 marked the high of the market for both new and 6-year-old 737-800s. Neither age was able to return to the market highs again, mostly due to the announcement and EIS of the MAX aircraft.

Value Retention

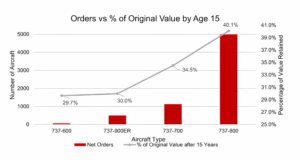

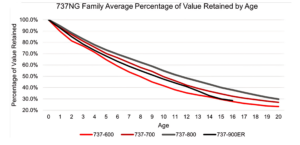

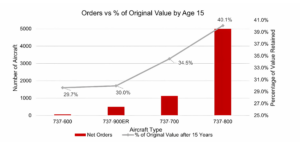

The 737-800 consistently retained more value over a 20-year period compared to the rest of the NG family, with 40% value retention after 15 years on average. The aircraft also has shown stronger retention compared to the A320-200 which has 32% of its original value on average at 15 years.

This can be mainly attributed to the diverse operator base and the large orderbook of the 737- 800 compared to other NG variants, making it the preferred type. Initial demand for freighter conversions also helped support value retentions while current passenger aircraft, spare engine, and spare parts demand have helped keep values strong as 737-800 converted freighter demand decreases.

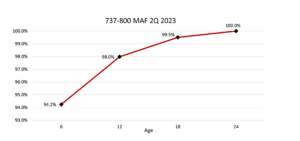

Pandemic Value & Trend Recovery

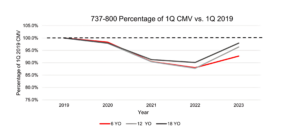

The 737-800 experienced moderate market volatility during the pandemic. Values decreased between 13.0% – 17.0% depending on the age but returned back to Base by July 2023, over three years since the triggering event. No long-term residual value impacts due to the pandemic are expected considering the aircraft has already made a full recovery even with its replacement, the 737 MAX 8 in service.

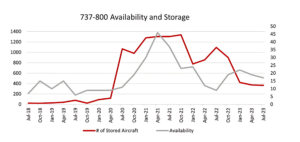

Value impacts were a result of high availability rates and a large portion of the fleet being parked due to the rapid decrease in domestic air travel demand. However, these impacts were softened for older aircraft as demand for narrowbody freighter conversions and spare engines increased. While freighter demand has ebbed, spare engine and part out value remains strong as well as passenger aircraft demand, aiding in the majority of the fleet in active service.

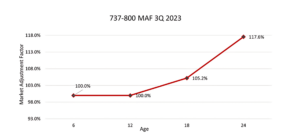

As of April 2023, 7.8% of the fleet was parked and though utilization is still below pre-pandemic levels where over 99.0% of the fleet was active, the remaining stored fleet continues to be reactivated. mba saw values move closer to Base in the beginning of 2023 and a full recovery realized by mid-2023. Though lease rates remain slightly below pre-pandemic levels, the demand for narrowbody passenger aircraft and high interest rates has aided in an uptick of values.

Current Trends

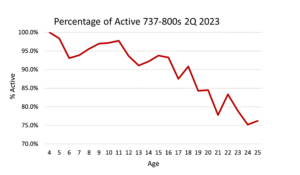

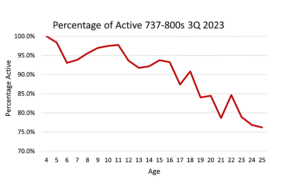

Older aircraft are trading closer to long-term residual values compared to younger aircraft, even though the number of stored aircraft increases with age. This is due to market values for older aircraft being supported by demand for spare engines as a result of significant backlogs for shop visits at MROs. A majority of the stored fleet is over 16 years old, however there has been a clear uptick in aircraft 16+ years old being reactivated between 2Q and 3Q 2023.

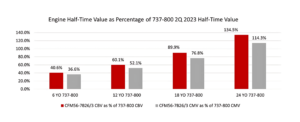

With values for the CFM56-7Bs rising in 2023 by around 8% from the beginning to mid-2023, after seeing further recovery through 2022, part out demand for older 737-800s remains high and can be a lucrative option for end of life aircraft.

Long-Term Outlook

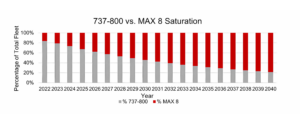

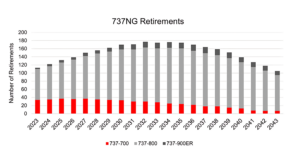

Due to the delivery delays and grounding, the 737-800 has a far greater percentage of aircraft in service versus the MAX. The MAX 8 is expected to reach ubiquity around 2029 based on current production rates while the 737-800retirements are forecasted to peak in the early to mid 2030’s.

The MAX 8 burns 14% less fuel than the -800, making it a much more attractive aircraft for operators from a fuel cost and sustainability perspective. However, increased maintenance costs on the MAX engines may make the NGs more attractive from an operational cost perspective if escalation continues at double digit rates and fuel prices remain below $100 a barrel. The MAX demand may see a surge if SAF becomes more prominent as the cost is slated to be around three times greater than jet fuel at the moment, providing significant cost savings with the MAX fleet compared to the NGs.

Long term value impacts and volatility will likely increase for the type as the MAX 8 becomes the dominant aircraft and the last off the line 737-800s enter into their mid to end of lives.

- Values will no longer be supported by freighter conversions if demand subsides, though feedstock will be plentiful as nearly 75.0% of the fleet is still younger than the prime conversion age.

- The lack of MAX 8s in service has aided the 737-800s residual values, allowing the near-term residual outlook to be positive, while in the long term mba expects to see the aircraft values depreciate faster and become more volatile, well into their end of life.