January 31, 2022

Alternative Collateral: Spare Parts Value Update

by Alex Cosaro, Director | Asset Valuations

As a leading provider of spare parts appraisals, mba Aviation (mba) has been closely monitoring spare part value trends during the ongoing pandemic. The pandemic had a significant negative impact on the values of spare parts servicing all aircraft types, however, using the A320ceo family as a case study, mba’s analysis shows there is reason for optimism that the Market Value for spare parts will recover close to pre-pandemic levels.

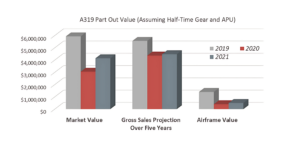

As seen in the graph below – in 2019, an A319 airframe traded from an airline, lessor, or financial owner to a part-out company within the range of $1.0-1.4 million, while the part out company could expect to gross just over $5.5 million in sales over 5 years in a piece part out scenario.

Source: mba Analysis, mba REDBOOK

By 2021, the value of an airframe dropped by upwards pf 60% to the $500,000 range and, based on mba’s forecasted spare parts demand and values, one can now expect to gross $4.0-$4.5 million in gross sales over five years in a piece part-out scenario. In this scenario mba anticipates depressed values in the near term with a Market Value recovery coming in the second half of the five-year sale period. Based this analysis, one can still expect roughly the same rate of return for an A319 purchased for part-out post-pandemic ($4 million net excluding consignment and repair costs) as pre-pandemic ($4.1 million net excluding consignment and repair costs).

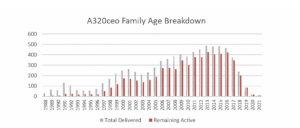

One reason to be optimistic about the A320ceo spare parts’ market is that the A320ceo fleet is relatively young with the active fleet having an average age of 11 years old, despite being first delivered to operators in 1988. This is mainly due to the approximately 3,500 A320ceo family aircraft delivered since 2011, accounting for 44.0% of all A320ceo deliveries since launch.

Source: mba REDBOOK Fleet

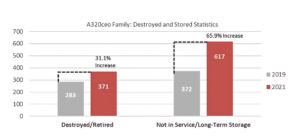

Short-term optimism for the A320ceo spare parts Market Value recovery can be generated by the fact that fewer A320ceo family aircraft have been retired and parted-out as initially feared when the pandemic began. Based on mba’s REDBOOK Fleet database, only 88 additional A320ceo family aircraft have been retired and scrapped since the 4th quarter of 2019. However, 245 A320ceo aircraft have been placed into long term storage due to the pandemic. The majority of these aircraft may return to service once pandemic conditions improve; however, these aircraft are likely to require significant airframe, landing gear, APU, and engine maintenance to return to active service, bolstering the market for spare parts for the type. In addition, there are over 1,000 A320ceo aircraft currently temporarily parked, with many of these aircraft requiring a C check at a minimum to return to service. This is also likely to increase the demand for spare parts over the next several years.

Source: mba REDBOOK Fleet

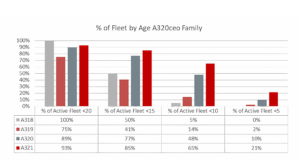

It’s important to note, the oldest A320ceo aircraft in the fleet (pre-1993 build) do not have enough parts commonality with newer A320 aircraft to yield similar gross parts values and are excluded from the value analysis. Of these newer aircraft, 77.1% have remained in active service during the pandemic, compared to only 16.8% of pre-1993 build A320ceo aircraft. The A320 and A321 freighter conversion programs have the potential to further boost demand for spare parts, much like the 737-700 and 737-800 freighter conversion programs, however the ratio of freighters converted vs aircraft manufactured will not be a significant factor in prolonging the aftermarket as was seen with the 757 and 767 spares market.

Source: mba REDBOOK Fleet, Airbus

The success of the A320neo allows for long-term optimism towards the A320ceo family spare-parts market. Airbus’ re-engine of the A320ceo, the A320neo, has generated strong sales as Airbus has booked 7,895 orders for the aircraft as of December 2021. With Airbus touting up to 95.0% spare commonality between the A320ceo and A320neo airframes, the success of the A320neo is likely to create strong demand for spares in the medium to long term and a healthy spare pool with limited bifurcation of parts between the two families.

The A320neo fleet is very young, with the average A320neo age being just over two years old. The average age of the fleet is likely to remain low as Airbus is currently planning to ramp up production of the A320neo family to 65 aircraft per month by 2023 and possibly up to 70 to 75 aircraft per month by 2025. Airbus originally planned to produce 63 aircraft per month by 2021, but these plans never came to fruition due to disruption caused by the pandemic perhaps creating additional A320ceo in-service fleet is large enough that the A320neo family will not go above 50.0% of the total in-service A320 fleet until 2027, which to put in perspective, equates to more than 4,000 aircraft. This is roughly equal to the sum of all 737-100/200, 737 Classics, 757 aircraft ever delivered.

Source: mba REDBOOK Fleet, Airbus

COVID-19 has had a significant impact on all aspects of aircraft values but due to the large and young remaining in-service fleet of A320ceo aircraft, the Market Values of spare parts for the family are likely to be resilient. the re-entry of stored aircraft into service is likely to generate demand for A320ceo spare parts in the short term, while the high degree of parts commonality with the A320neo family could keep demand high in the long term. Excluding any unforeseen extension of pandemic related travel restrictions globally, mba expects the Market Values of A320ceo spare parts to approach 2019 levels by 2024, with airframe values following shortly thereafter.

If you have any questions, comments, or would like to discuss any of the above topics in more detail, please contact mba Aviation’s appraisal team at appraisals@mba.aero.