August 9, 2021

CFM56-5B Market Insight

by Garrick Rice

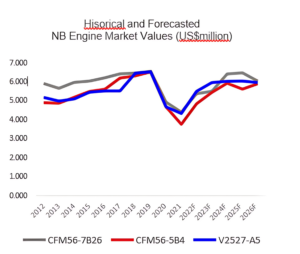

Domestic air traffic volumes have been steadily climbing from the lows experienced in 2020, and narrowbody engine Market Values have seen stability as a result. Historically, narrowbody engine values have seen little variance between types that power the 737NG and A320ceo fleets, but differences in global responses to the pandemic and maintenance issues have seen different Market Value dynamics between the types.

Value decline in the CFM56-7B market has been counteracted by the robust traffic rebound in the U.S. and Chinese domestic markets where 737NG concentration is high, along with freighter conversion application. The V2500-A5 value declines have also been counteracted by an AD that has proved positive for Market Values for the engine as leasing demand has seen a sudden increase to limit aircraft downtime during the recovery period. In January 2021, the FAA issued AD 2021-01-03, which required certain disks in the V2500-A5 engine to be removed from service within 50 Flight Cycles (FC) due to a manufacturing anomaly. The affected population was small, with 20 HPT-1 and eight HPT-2 Disks affected. Subsequently, the FAA issued Emergency AD 2021-11-51E, requiring removal of seven HPT-1 and eight HPT-2 disks within ten FC. It’s not known at this point how many engines will be subject to a removal requirement, but airlines have begun to prepare for high amounts of these affected engines to require maintenance.

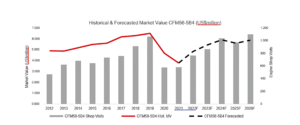

The CFM56-5B market, however, has been slightly depressed compared to the CFM56-7B and V2500-A5 markets during the time after the initial pandemic response. There is a high concentration of Airbus aircraft in Europe, India, and South America, where a lack of vaccine distribution and increased COVID-19 variants have continued to limit meaningful traffic recovery to 2019 levels; however, as European travel markets begin to increase available seats and discontinue quarantine measures, this decline in Market Values is not expected to continue. Engine shop visit forecast are expected to increase substantially starting in Q4 2021 and continue to increase year-over-year until they peak in 2026. As a result, Market Values are expected to steadily climb as consumption of unserviceable engines and spare engine leasing demand increase as a result of overdue MRO activity. Using mba’s engine shop forecast, Market Values are expected to return to projected Base Values as shop visit totals near the highs seen 2018–2019.